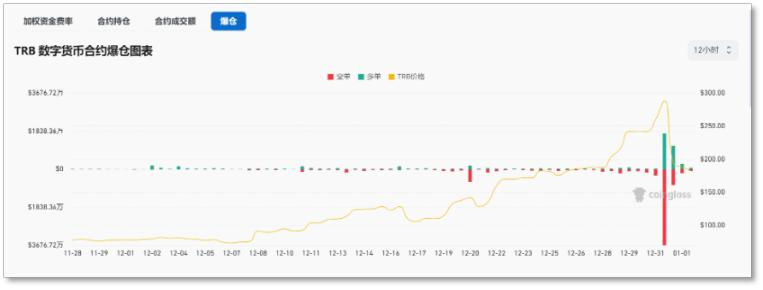

The violent fluctuations in a short period of time directly caused the "double explosion of long and short" in the contract market. Data shows that in the 24 hours before 8 a.m. on January 1, the liquidation amount of the TRB futures contract was US$ 73.1 million, of which short positions were liquidated at US$ 44.49 million and long orders were liquidated at US$ 28.61 million.